Albo, or Plibersek, or whoever turns out to be the next Labor leader, might have had a lucky accident. Usually, it’s Labor that inherits an economy turning down.

This time, it’s the Coalition. And because of regular updates from the Reserve Bank and the Bureau of Statistics strikingly at odds with their public position that the economy is strong, they ought to be finely attuned to it.

Economic growth, the catch-all that is supposed to show us where the economy has been and where it is headed, is frighteningly small.

The Treasury’s best estimate of potential growth – how strongly the economy could be growing over time if things were well managed – is 2.75% per year.

The reality, for the two most recent quarters for which we have data, is 0.3% and 0.2%.

The economy is anaemic, despite the crowing

If you add those two numbers together and multiply by two you discover that for six months the economy has been growing at an annualised pace of just 1% – way, way short of its potential.

Stripping out population growth and minimal price growth, real living standards have been going backwards.

The bank says consumption growth has slowed most noticeably for discretionary items that tend to have the strongest relationship with home buying, such as furnishing and household equipment. It says growth in other types of discretionary spending, such as eating out, has also slowed. Consumption of so-called “essential” items is holding up.

We’re going to need a boost

It means we can’t rely on household spending to revitalise the economy (although the government will give it a go, stumping up a bonus of as much as $1,080 to be delivered with each tax return from July in a much-needed boost that will be disguised as a tax cut rather than spending).

Household spending accounts for three-fifths of gross domestic product. The bank identifies uncertainty over household spending, which itself derives from uncertainty over income growth, as a “key risk” for economic growth:

Should households conclude that low income growth will be more persistent than previously expected, households may adjust their spending by more than currently projected and consumption growth could remain weak for a longer period.

Labor would have helped stabilise uncertainty over income growth by immediately intervening before the Fair Work Commission to get higher wages, directing it to draw up a long-term strategy for higher wages, restoring cut penalty rates, and funding the increases of some childcare workers itself.

Having won an election opposing those things, the Coalition will have to try other things, perhaps even bigger and earlier tax cuts.

Prayer would help – prayer that international commodity markets remain strong, that the Reserve Bank cuts rates on June 4 (it is practically certain to), that it cuts them again before the end of the year (financial markets are literally 100% certain that it will) and that home prices stabilise.

Perhaps a very big boost

On the face of it, none of these would be enough to force economic growth back up. If it falls even further and continues to fall, Australia will enter a recession within this term of government, an outcome to which the academic economists polled by The Conversation in January assigned a 25% probability.

So far employment growth has been the economy’s brightest light, but in its quarterly update released a week before the election the Reserve Bank pointed out that employment growth can lag economic growth by up to nine months, meaning it might be about to turn down, although it added that it was not unusual for “trends in GDP growth and the labour market to diverge for sustained periods”.

If employment growth does turn down (and the bank says “near-term leading indicators of labour demand have softened”) it is likely to happen first in the construction and retail industries. The construction jobs will come again (and the government is doing its best to bolster them with promises of spending on infrastructure) but the retail jobs might never return, the nature of retailing having changed.

The economy matters more than the surplus

If needed in order to avoid a recession the government will have to be prepared to abandon its promised 2019-20 budget surplus. If the prospect of a recession does loom, it’ll have the political cover. And if it looms early in its term, it might still be able to deliver a budget surplus by the end.

Scott Morrison and his treasurer, Josh Frydenberg, were elected to manage the economy, and that means doing whatever is needed to avoid a recession and the long-term damage to lives and living standards it would deliver.

Speaking personally, I’ve no doubt they are up to the task, just as Labor would have been. In a way it’s a pity they didn’t adopt one of Labor’s key economic promises, which was to have a new budget in August, to refresh things.

And it matters more than superannuation

And they’ve got to focus on lifting living standards over the longer term where, conveniently, they have a big advantage over Labor.

Labor has a blindspot when it comes to superannuation. It wants to lift compulsory contributions from 9.5% of salary to 10% on July 2021, and then by another 0.5% the next year and another 0.5% the next year and so on for five consecutive years, apparently regardless of what it will do to incomes now.

It’s a good thing that, unlike Labor, the Coalition will be relaxed about pushing out the timetable if the economy can’t stand it, as it has done before.

Before the election it was preparing to respond to the landmark Productivity Commisson report that found that unintended multiple accounts and the defaulting of new workers into entrenched underperforming funds were costing members an extraordinary A$3.8 billion per year.

The Coalition can set up super for the future

Weeding out the chronic underperformers, clamping down on unwanted multiple accounts and insurance policies, and letting workers choose funds from a short menu of good funds and stay in them for life would give the typical worker entering the workforce an extra A$533,000 in retirement.

Is there a “big black hole” in Labor’s election costings? It’s unlikely.

The final campaign before the arrival of the Parliamentary Budget Office in 2012, the 2010 Gillard versus Abbott contest, was full them.

Abbott was in opposition, Joe Hockey was his treasury spokesman. A treasury analysis of the costings document he produced, delivered to the newly-elected independent members of parliament to help them decide who would form government found errors including double counting, purporting to spend money from funds that sweren’t there, using the wrong time period to calculate savings, and booking debt interest saved from a privatisation without booking the dividends that would be lost.

All up, the mistakes were said to amount to A$11 billion.

Opposition costings used to be awful

In order to give his calculations a veneer of respectability Hockey engaged two accountants from the Perth office of a firm then known as WHK Horwath and wrongly said they had audited them.

“If the fifth-biggest accounting firm in Australia signs off on our numbers it is a brave person to start saying there are accounting tricks,” he told the ABC. “I tell you it is audited. This is an audited statement.”

It wasn’t. The letter of engagement later seen by Fairfax Media explicitly said the work was “not of an audit nature”. Its purpose was to “review the arithmetic accuracy” of Hockey’s work.

Three years on, with the Parliamentary Budget Office in place, Hockey’s costings were comparatively controversy-free, as were Chris Bowen’s when Labor was in opposition in 2016.

Now, they’re fairly controversy-free

Costings have become straightforward. The Parliamentary Budget Office prepares the best possible estimate of the cost of each policy, then a panel of eminent Australians goes over its calculations and adds the costs together.

Labor’s panel this time was the same as its panel last time: Professor Bob Officer, who chaired the commissions of audit for the Howard and Kennett Coalition governments, Dr Michael Keating, who used to head the department of prime minister and cabinet and finance under the Hawke and Keating governments, and company director James MacKenzie.

They provided “a reasonable basis for assessing the net financial impact on the Commonwealth budget”.

Labor’s costings are propped up by savings

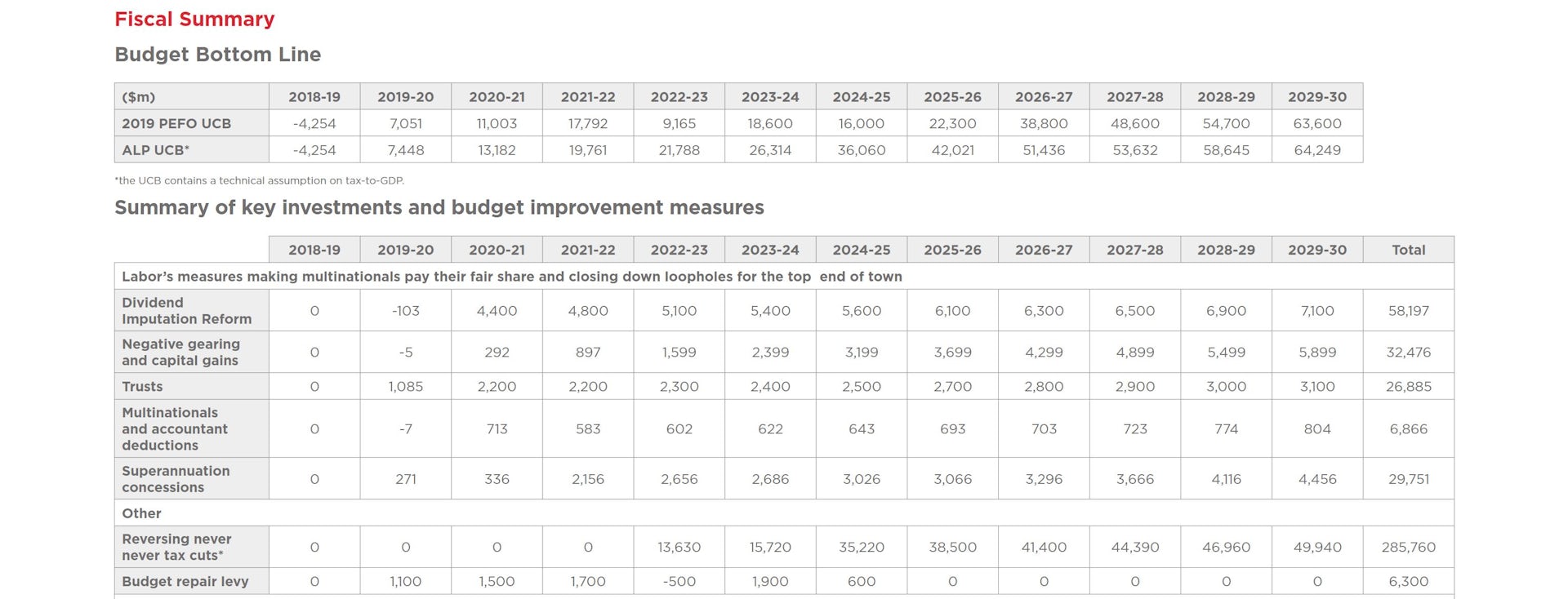

That impact was a return to “strong surplus” of $22 billion under Labor in 2022-23, four years ahead of the Coalition, in a year which the Coalition is forecasting a surplus of less than half the size – $9.2 billion.

Labor is able to do it because it will raise (or avoid spending) more than the Coalition. Over ten years it will save

$58 billion by winding back payouts of dividend imputation cheques to people who don’t pay tax

$32.5 billion by winding back negative gearing and capital gains tax concessions

$29.8 billion by reducing superannuation tax concessions

$26.9 billion by more fully taxing trusts

$6.9 billion by cracking down on multinational tax avoidance and the use of high fees for tax advice as tax deductions, and

$6.3 billion from reintroducing for four years the Coalition’s temporary budget repair levy of 2% on the part of high earners’ income that exceed $180,000

Treasurer Josh Frydenberg attacked the costing saying Labor had confirmed “$387 billion in higher taxes; higher taxes on retirees, higher taxes on superannuants, higher taxes on family businesses, on homeowners and renters and low-income earners,” which it had, although it had hardly been a secret.

The tax measures are how Labor builds its bigger surpluses.

The best an opposition can produce

Frydenberg said Labor had failed explain the “economic impact these higher taxes will have across the economy”, a charge Labor had responded to earlier by saying that wasn’t a service the Parliamentary Budget Office provided.

It was work the treasury was able to do, but the resources of the treasury weren’t available to the opposition.

Besides which, a fair chunk of those savings would be spent, on programs such as Labor’s Medicare cancer plan, its pensioner dental plan, extra hospital funding and greater childcare subsidies. They would boost the economy.

Unlike the Coalition, Labor isn’t locking in tax changes years out into the future (although its costings set aside $200 billion for extra tax cuts at some point over the next ten years); it is giving itself flexibility in order to manage the economy as needed when the time came.

Frydenberg identified as the “big black hole in Labor’s costings”, what he said was its “failure to account for the increase in spending that they have promised with changes to Newstart, to aid, to research and development”.

Four years out is conventional

It wasn’t much of black hole. Labor has not promised changes to the Newstart unemployment benefit – it has instead promised to review it. Without the result of the review or without an indication of how much Newstart might be lifted or when it would be lifted, it’d be a hard thing to cost.

Frydenberg’s other beef was with programs Labor’s document costed in detail for four years but not in detail for ten. But that is how his own budget presented its figures. It’s how every previous budget has presented its costings.

Since the late 1980s it’s been the convention to cost programs in detail only four years ahead. Before that, the budget convention was to cost programs in detail only one year ahead.

It is possible that Labor’s costings document is less than perfect. It is possible that the three eminent Australians who lent their names to it have been hoodwinked. But the contours of the document are clear. Labor will tax more and spend more than the Coalition, and deliver bigger surpluses.

But it only plans to tax more up to a certain point: 24.3% of gross domestic product, which was the tax take in the final year of the Howard government. The Coalition’s limit is 23.9% of GDP, which will mean it finds it harder than Labor to build up a big surplus quickly.

The days of black holes are behind us, thankfully.

On Friday morning the Coalition’s worst dream will come true.

All throughout the campaign, and all through the two terms in office and three prime ministers and three treasurers who preceded it, they’ve argued they are better than Labor at managing money. They had budget surpluses under Howard that Labor didn’t have under Rudd and Gillard.

In the last election, Labor allowed them to get away with it. Its costings document actually forecast a better budget position than the Coalition’s over ten years (because it rejected the Coalition’s expensive company tax cuts) but a worse position over the immediate four-year “forward estimates”, because of its more generous programs.

The Coalition focused on the four years, not the ten, and painted Labor as irresponsible.

Bigger, sooner surpluses

On Friday morning, Labor won’t make the mistake again. Yes, it’ll detail (and have year-by-year costs for) programs that are more generous than the Coalition’s, among them cheaper childcare, its Medicare cancer plan and its pensioner dental plan.

But it’ll be able to more than pay for them in every one of the next ten years because of a number of courageous decisions that’ll save money, the most financially important of which is the decision to stop sending company tax refund cheques to people who don’t pay tax. It’ll save A$5 billion in the first year and more in future years because the cost of the refunds has been ballooning.

The result will be a larger budget surplus in every one of the next ten years, including each year of the forward estimates and including the financial year about to start, which is when the budget is scheduled to return to surplus.

So big will be these bigger surpluses that Labor has its budget on track to hit the Coalition’s target of 1% of gross domestic product four years earlier than the Coalition in 2022-23 rather than 2026-27.

That means that in Labor’s first budget, which it will deliver in August this year if elected as a means of resetting forecasts, its projections will show the long-awaited surplus of 1% of GDP within the forward estimates, rather than beyond them as in the Coalition’s budget.

Labor’s 1% of GDP will be A$22 billion, twice the surplus of $9.2 billion the Coalition plans to deliver in that year.

All Labor needed was courage, and the ability to withstand complaints from people who own shares but don’t pay tax and are naturally upset about losing government cheques they’ve become used to.

And lower government debt

Bigger surpluses and the much more rapid delivery of a substantial surplus will mean much quicker reductions in government debt. The budget had the government on track to eliminate net debt by 2030. Labor’s costings will have it on track to eliminate it much sooner.

Despite what the Coalition would like to claim, the key reason Labor’s surpluses will be bigger isn’t that Labor won’t be matching its longer-term tax cuts. Bracket creep means tax rates need to be cut or thresholds adjusted from time to time to ensure the personal tax take doesn’t climb too high. Labor’s costings recognise this, including a built-in assumption of tax cuts after the tax take hits 24.3% of GDP, a figure cunningly selected because it was the tax take when Howard left office.

If delivered as income tax cuts, at about the time the Coaltion’s high-end tax cuts are due, it’ll cost A$200 billion, but the method of delivery will depend on circumstances at the time.

With future tax cuts baked in

Labor’s “technical assumption” that the tax take won’t climb beyond 24.3% of GDP is different to the Coaltion’s “guarantee” that it won’t climb beyond 23.9% of GDP. It is a technical assumption rather than a promise, of the kind usually included in budget documents as a way of allowing for inevitable future tax cuts.

Without it, Labor’s surplus projections would have been much bigger and would have been hard to believe. With it, the projections should be credible.

The secret sauce in Labor’s better budget projections isn’t that it isn’t adopting the Coalition’s tax cuts. It is that it’s tackling the handing out of billions of dollars in dividend imputation cheques to people who don’t pay tax in a way the Coalition wasn’t prepared to.

Not that it didn’t think about it. A file list seen by Fairfax Media shows Treasury created a file entitled “Tax Policy - Dividend Imputation” in the lead-up to then Treasurer Scott Morrison’s 2017 budget.

The tax reform discussion paper commissioned by his predecessor, Joe Hockey, found “revenue concerns with the refundability of imputation credits”.

Expect to hear a lot about tax during the coming leaders’ debates.

Which is why it’s important to get two things straight.

The first is that you can’t argue against a tax by pointing out that it will take money from people.

By all means, use that as an argument against taxes in general. It’s true – taxes take money from people. But to oppose better taxing capital gains or tightening up on dividend imputation refunds because they will take money from people is to leave unexplored the more important question of whether those particular tax measures are better or worse than the alternatives.

You can’t escape that question by just saying that all taxes are bad – that we ought to collect less. For any amount of tax collected, the next most important question is the way in which it is collected.

Low tax and high spending can be the same thing

And the second thing we ought to get straight is that talk about one side of politics being “low tax” and the other being “high tax” tells us next to nothing.

To see this, consider Bill Shorten’s childcare policy announced on Sunday. Labor has promised to spend A$1 billion a year in subsidies to cut the cost of childcare for every family with a combined income of up to $175,000 and to make it free for working families earning up to $69,000.

But what if, instead of subsidies, it had promised to deliver the $1 billion via tax rebates, to be paid to parents on proof of their use of childcare?

The effect would be same, although the method of payment would be more complicated.

Childcare would be just as supported, and just as supported from the public purse, but one policy would be called “big spending”, while the other would be called “low tax”.

Take the quiz

Here’s a quiz: is the Private Health Insurance Rebate a tax break (and counted in the budget as a contribution toward lower taxes and smaller government) or is it a spending measure (and counted in the budget as boosting the size of government)?

What about the Family Tax Benefit? Or the film industry tax rebate or the seniors And Pensioners Tax Offset or the Low Income Tax Offset or the existing Child Care Rebate?

It’s okay. You’re not expected to know. The answer varies from case to case. The point is that it is silly to claim that tax cuts are good, and government spending is bad, when in many cases each could be easily classified as the other.

The signature measure in the April budget is a case in point. It’s a tax offset of up to $1,080 per person to be paid out with tax returns after July 1. It’ll push billions into the economy, just as the Rudd government’s cash bonuses during the global financial crisis did. But Rudd’s payments were categorised as spending; these payments will be categorised as tax cuts, which means they will keep down the tax-to-GDP ratio.

Which means it is silly to talk about the tax-to-GDP ratio, as the government insists on doing.

That speed limit, where did it come from?

Labor was keen enough to do it while it was in office, boasting in its final budget in 2013 that its tax-to-GDP ratio was lower than in the Howard years, and lower than it had been before the global financial crisis, as if that was an achievement to be proud of. It wasn’t. The ratio was lower than during the mining booms because fewer tax dollars were rolling in, and it was lower than before the financial crisis because the economy was weaker.

The Coalition has hardened the tax-to-GDP ratio into a target. As treasurer, Scott Morrison spoke last year of “a speed limit on taxes in our budgets, that requires that taxes do not grow beyond 23.9% of our economy”.

Why 23.9%? Well, in the Coalition’s first budgets it wasn’t a target at all, merely an operating assumption used by the treasury for long-term forecasting. As it explained in the 2017 budget papers:

A tax-to-GDP “cap” assumption is adopted for technical purposes and does not represent a government policy or target. It is based on the average tax-to-GDP ratio over the period from the introduction of the GST and to just prior to the global financial crisis.

Treasurer Josh Frydenberg and Finance Minister Mathias Cormann have begun talking about 23.9% as if it’s a commitment, a pledge, even though it would be hard to keep if the economy picked up (and probably unwise to keep), and even though it is fairly meaningless given the ease with which changes in spending can be classified as changes in tax and the other way around.

Treasury makes pretty clear what it thinks about the measure in the back of Budget Paper 1. That’s where it sets out the history of the important budget measures and its forecasts for the future. You won’t find the tax-to-GDP ratio in the first two tables. Instead, it details “revenue to GDP”, which is a much more relevant measure because it includes income from all sources – fees as well as taxes, and income from Future Fund earnings which are revenue too.

Think like treasury

Early in his time as time as shadow treasurer, Labor’s Chris Bowen bought into tax-to-GDP debate, challenging the Coalition to keep the ratio below such and such per cent. He isn’t doing so now.

It’d be wise to ignore talk of the tax-to-GDP ratio in the coming leaders’ debates

Focus instead on what they’re planning to do and how they are planning to pay for it. You’ll get a handle on how to vote.

Some of it involved tax cuts way out into the future, in 2022 and 2024, with which we needn’t concern ourselves – there’ll be two, maybe more, elections before then.

The bit that was to start in mid 2018 (and did) wasn’t a tax cut at all, strictly speaking. It was an “offset” with an ungainly name: LMITO – the Low and Middle Income Tax Offset.

A standard tax cut, applying to any rate, would save money to all taxpayers on that rate and rates above it, including those on very high incomes. It couldn’t be directed to just low and middle earners, which is what the Coalition wanted.

What’s on offer isn’t really a tax cut

So the Coalition designed an offset, to be paid as a lump sum after the end of each tax year, after returns had been submitted and only to those taxpayers whose returns showed they weren’t high earners.

The full offset was A$530 per year, paid only to taxpayers who earned between $48,000 and $90,000. Taxpayers who earned more than $90,000 would lose 1.5 cents of it for each dollar they earned above $90,000, meaning no-one who earned more than $125,333 would get any of it.

(Taxpayers earning more than $125,333 wouldn’t go home completely empty handed - they would benefit from an increase in the point at which the the second highest rate came in, worth a barely consequential $135 a year.)

Taxpayers who earned less than $37,000 would get $200 off their tax, climbing to $530 for taxpayers earning $48,000.

It was ungainly – it was better described as a series of annual lump sum payments than a tax cut – and Labor embraced it entirely.

In 2018 Labor trumped it

Except that Labor supercharged it. Under Labor it was to operate in exactly the same way, except that each payment would be 75% bigger: the Coalition’s $200 became Labor’s $350, the Coalition’s $538 became Labor’s $928 and so on.

Labor outbid the Coalition.

And these things stayed, for almost a year, except that it was all a bit academic.

Labor wasn’t in government, and the leglislated offsets weren’t to put the lump sums in pockets until after the end of June 2019.

In 2019 the Coalition trumped Labor

It allowed the Coalition to sneak in before them in Tuesday’s budget and double the maximum lump sum: $538 became $1,080, a promise Bill Shorten matched in his budget reply speech on Thursday night.

But for some reason the Coalition didn’t double everything: $200 only became $255, rather than the $350 Labor had already promised.

On Thursday night Shorten confirmed the $350 promise.

He is able to offer the 3.6 million Australians earning less than $48,000 more than the Coalition – in most cases an extra $95 more: $350 instead of $255.

Now Labor has trumped the Coalition

Shorten says it’ll cost an extra $1 billion over four years, which is a mere fraction of the money Labor believes it will have that the Coalition won’t, because of its crackdowns on negative gearing, capital gains tax concessions and dividend imputation.

As Shorten put it on Thursday night:

Labor will provide a bigger tax cut than the Liberals for 3.6 million Australians all-told, an extra $1 billion for low income earners in this country. Here’s the simple truth - 6.4 million working people will pay the same amount of income tax under Labor as the Liberals. Another 3.6 million will pay less tax under Labor.

In fact they’ll pay just as much tax from payday to payday, but they’ll get back more at the end of the year, in most cases $95 more.

Talk about retrospective. In his determination to quickly inject money into the economy (for economic as well as political reasons), Treasurer Josh Frydenberg has reached back in time to give us an extra tax cut on income already earned during the financial year that’s about to finish.

Almost a year ago, in May 2018, Frydenberg’s predecessor, Scott Morrison, promised a “sort-of” tax cut for the financial year beginning in July 2018. People earning between A$48,000 and A$90,000 would get a tax offset – a bonus – of $530 as part of their tax return.

People earning more, or less, would get lesser amounts but would still get something, right up to a cutoff of $125,333.

The arrangement meant they wouldn’t get the money until the following financial year, the one beginning this July, after they submitted their tax forms.

Now Frydenberg has trumped Labor and Morrison, announcing a rebate of almost twice the original size — $1,080 — to be paid out after the end of the financial year.

But, in an innovative piece of policy, he is applying the increased offset to the financial year that’s almost over, as well as the ones to come. It means that after submitting their tax forms for the financial year that’s about to end, most Australians will get $1,080 back for the work they did during 2018-19, instead of the $530 that was promised at the time (assuming the measure is enacted).

It will work the same way as the Rudd government’s “cash splash” during the global financial crisis. It’ll be paid into bank accounts within weeks, providing near-instant, much-needed spending power.

The fact that it will be bigger than the first Rudd government cash splash (which was $800 for qualifying taxpayers) is probably no bad thing.

It’s what we need, unfortunately

Consumer spending is much weaker than was expected in the December budget update just five months ago, and a lot weaker than was expected in Morrison’s last budget as treasurer a year ago.

Morrison expected consumer spending to climb 2.75% for 2018-19. Frydenberg cut that forecast to 2.5% in December and to 2.25% today.

Morrison expected consumer spending to climb 3% in 2019-20, and Frydenberg held the line in December. Now he has marked down the 2019-20 forecast to 2.75%. He has also marked down (yet again) the forecasts for wage growth and economic growth.

Home prices, not explicitly forecast in the budget, are also lower than was expected in the last budget and budget update. Along with lower-than-expected wage growth, this is depressing consumer spending.

The markdowns in spending, wage growth and economic growth have started to hurt revenue forecasts, but the damage isn’t yet apparent because at the same time dramatically higher iron ore prices have been pouring more money into the budget than was expected.

When iron ore prices fall, we’ll be exposed

When, for whatever reason, the higher iron ore prices recede (and that’s what the Treasury says it is expecting), the budget will look much worse. Unless consumer spending and wages pick up, which is also what the Treasury says it is expecting, in the face of evidence to the contrary.

That’s what makes Frydenberg’s cash splash so important. It will push an extra $3.5 billion into the economy within weeks. On top of it will be an extended instant asset write-off for small and medium-sized businesses, the operative word being “instant”.

From now on, businesses with a turnover of up to $50 million (up from $10 million) will be able to buy equipment worth up to $30,000 (previously $25,000) and deduct the full cost from the tax they will owe from July.

The measure won’t cost the government money until next financial year, but it will inject money into the economy from Wednesday in the 14 weeks before that financial year starts, as as many as 22,000 previously ineligible businesses spend up to $30,000 on equipment (even cars) and then spend it again and again without limit.

A peculiarity of the instant asset write-off is that businesses can spend as much as they like and get it all back, as long as it is broken up into parcels of less than $30,000. In an example quoted in the budget papers, a previously ineligible food manufacturing business buys ten new commercial ovens, each for $12,000. The entire $120,000 can be written off within weeks, helping the business “invest, grow, and employ more workers”.

Frydenberg would probably prefer it if the measures weren’t called “stimulus” measures, but that’s what they are. And they are needed, for economic reasons as well as for political ones.

The economists surveyed in January for this year’s Conversation economic survey assigned a 25% probability to a recession within the next two years. The downward revisions in the budget have done nothing to change that assessment.

The government elected in May will inherit a fragile economy in need of help.

Frydenberg has demonstrated that he is just as prepared as was Kevin Rudd during the global financial crisis to provide it.

The Coalition is running out of time to do worthwhile things.

Facing overwhelming odds of defeat in the election due within weeks, one of its last throws of the dice should be to do something Labor would never do, but which is urgently needed and would set us on the right course for the future.

It’d also cause some trouble for Labor along the way.

It is to launch a full-blown inquiry into the superannuation system Labor has lumbered us with.

It’s urgent because compulsory super contributions are scheduled to climb from the current 9.5% of salary to 12%, beginning with an increase of 0.5% in July 2021, followed by an extra 0.5% in 2022, 2023, 2024 and 2025.

Under the schedule imposed by Labor when it was last in office compulsory contributions were to climb by 0.25% of salary in each of 2013 and 2014 and then at twice the rate, by 0.5%, in each of the five years after that.

Compulsory super is set to jump..

The Coalition hit pause after 2014 just before the rate accelerated, postponing the series of five much bigger increases until 2022, when it might have hoped that wage growth would be robust enough to cope with it, or when it would have been someone else’s problem.

Labor says it will stick to that schedule, presumably regardless of wage growth or other economic conditions or the need for extra super contributions at the time.

Asked, ahead of the release of the Productivity Commission’s report on how to make super funds more efficient, whether Labor would reconsider the schedule if the Commission found other ways to boost retirement incomes, Labor Treasury spokesman Chris Bowen said it would not.

It’s almost as if – to Labor – lifting compulsory super contributions has the status of a holy writ; perhaps because it would “complete the work” of Labor elder statesman Paul Keating who introduced compulsory super, or perhaps because so many union officials are tied up with the running of the funds that would benefit from the schedule of increases.

In the event the Productivity Commission report released on January 10 found ways to massively lift retirement incomes without lifting super contributions.

…whether we need it or not

It found unintended multiple accounts and the defaulting of new workers into entrenched underperforming funds were costing members an astonishing A$3.8 billion per year.

Weeding out the chronic underperformers, clamping down on unwanted multiple accounts and insurance policies, and letting workers choose funds from a short menu of good ones and stay in them for life would give the typical worker entering the workforce an extra A$533,000 in retirement.

Even a typical worker aged 55 today would get an extra A$79,000 in retirement.

What the Commission’s report couldn’t say, but stongly implied, was that if the Commission’s recommendations were adopted an increase in costly compulsory contributions might not be necessary.

Its terms of reference limited it to assessing the “efficiency and competitiveness” of what happened to the contributions that were collected.

Henry was unconvinced

Another inquiry – less hamstrung – was the Henry Tax Review. It found no need to increase contributions. Labor treasurer Wayne Swan dishonoured its findings by announcing the proposed increase in contributions on May 2, 2010, the day he released its report.

But super wasn’t the main focus of the Henry Review. In the 25 year history of compulsory super, there has never been an inquiry into what the rate should be and what the system has achieved. It’s as if governments of both types have been keen to govern blindly.

So in January the Productivity Commission tentatively ventured beyond its brief, in a recommendation Treasurer Josh Frydenberg has promised to respond to before the election.

It is Recommendation 30, for an independent inquiry into the entire system.

The independent inquiry would determine whether or not the system we’ve had for the past 25 years has boosted national or even private savings rates, as well as who it has hurt and who it has helped.

They are the type of questions you would think a government would want to answer before lifting compulsory contributions further from 9.5% of salary to 12%.

Frydenberg could show leadership…

Indeed, Recommendation 30 explicitly asks that the inquiry “be completed in advance of any increase in the superannuation guarantee rate”.

It is possible to guess what the inquiry would find:

that almost all increases in employers’ compulsory super contributions come out of what would have been wages, depressing workers take home pay, a finding that will not be seriously disputed

that the system hasn’t boosted national savings - the increase in private savings has been offset by the decrease in government savings brought about by the use of the super tax concessions

that the increase in private savings has come almost entirely from the middle to low earners who have been unable to escape the impact of the levy, because they have had no other savings they could cut. They are the people who could least afford to save more at the time they were forced to

the tax benefits have gone overwhelming to the high earners who are saving no more than they would have without them, and without compulsion

In sum, the inquiry is likely to find that the system is regressive and cruel. Or perhaps not. We won’t know until it is held.

It ought to be conducted by an expert panel whose members are highly respected and who will amass evidence the next government won’t be able to ignore.

…ensuring Labor does more than look after mates

Frydenberg ought to appoint the panel now, or within weeks, so that an incoming Labor government can’t dismantle it.

It would be one of his most important legacies. And would give him something to press the next government about should he be in opposition.

In time an incoming Labor government might thank him.

At present, without the scheduled increases in compulsory super, wage growth is just 2.3%. With the scheduled increases of 0.5 percentage points per year, wage growth might fall below the rate of inflation, for five consecutive years.

No sensible treasurer would allow that happen. By doing what’s right, Frydenberg might be giving Bowen an out.

Newspapers need to economise on words. Television and radio reporters need to economise on seconds. So they use shorthand: words like “dividend imputation”, “franking credits”, and yes, “retiree tax”.

Which is fine if you already know what they mean, and pretty fine if you don’t, because you probably don’t need to. They speed things along.

Until now. Suddenly, because of their prominence in the upcoming election campaign, we are going to have to know what they mean. We are even going to have to know that one of them doesn’t mean what it seems to mean. The election might depend on it.

So here goes:

Taxable profits

If a company’s income exceeds its expenses, it has made a profit, which in ordinary circumstances is taxed at the legislated rate, which for big companies such as Telstra and the big banks is 30 cents in the dollar.

Dividends

After the tax is taken out, companies can pay some of what’s left to shareholders as a dividend, one for each share.

Last September Telstra paid shareholders a dividend of 15.5 cents per share. The previous March it was 11 cents.

Income tax

Australians pay tax on what they earn, unless the income is classified as not taxable or is below the A$18,200 tax-free threshold. The marginal rate (the rate on extra income) climbs with income, so that anyone earning more than A$180,000 (the top threshold) pays 45 cents on each extra dollar earned.

Dividends are taxable and so are taxed along with other income.

Dividend imputation

In 1987 in what he hailed as a world first, Labor treasurer Paul Keating introduced a rebate for each each tax-paying dividend recipient.

Taken off their tax would be the company tax the company had paid on the part of the profit that had been handed to them as a dividend.

It would greatly reduce the existing bias in the tax system which

taxed interest income once, but dividend income twice.

Here’s how it would work at today’s tax rates.

Jill owns 1,000 Telstra shares

Over the period of a year she gets dividends of A$265

To provide them, Telstra made a profit of A$379 on which it paid A$114 tax

Jill pays tax on the full $379 but gets a credit of A$114 that can be taken off any other tax she owes that year

As with other tax credits, it can be used to cut Jill’s tax bill as far as zero, but not to turn it negative. It can’t be handed to her in cash.

As Keating put it, the tax paid at the company level would be imputed, or allocated to shareholders by means of imputation credits.

But not to all of them. Non-resident (overseas) shareholders couldn’t get them, and nor could shareholders whose dividends hadn’t been franked.

Franking credits

As Keating explained, the tax credit only applied to the extent to which full Australian company tax had been paid; to the extent to which the dividends had been franked (stamped) to indicate that tax had been paid.

Not every company pays the full 30 cents in the dollar in every year. Often it is carrying forward previous losses. Only dividends from profits on which full tax had actually been paid were to be marked “fully franked”. Dividends on which tax had been partly paid were to be marked “partly franked”.

Fully franked dividends became sought after, because they brought with them the biggest franking credits. In a useful side effect, dividend imputation encouraged companies that wanted to look after their shareholders to pay full tax.

Refunds to non taxpayers

Although the particular Australian design arguably was a world first, dividend imputation or something similar is not unusual. Many countries have systems in place that to a greater or lesser degree ensure company profits are taxed only once – among them Canada, New Zealand, Chile, Mexico, Malaysia and Singapore, whose system is called “one-tier” tax.

Many that did adopt it later moved away from it, using the money saved to cut headline tax rates; among them Britain, Ireland Germany and France.

What is unusual is what Australia did next. In 2001 after more than a decade of dividend imputation, the Howard government supercharged it, paying out franking credits in cash to shareholders who didn’t have any or enough tax to offset.

From the point of the view of these non-taxpayers, dividend imputation became a negative income tax: instead of them paying the government money, the government paid them money.

As far as is known, it is an enhancement that has not been copied anywhere.

On one hand, it makes sense because it treats non-taxpayers the same as taxpayers by refunding them the same amount of company tax.

On the other hand, it does not make sense because it means that instead of being taxed once (at either the company or the personal level) as was the original intention, company profits can escape tax altogether.

Untaxed super

From 2007 the change mattered to many more retirees.

The Howard government’s “Simplified Superannuation” package made super benefits paid from a taxed source (that’s most super benefits outside of the public service) tax free when paid to people aged 60 and over.

A quirk in the wording of the Act went further. Not only did super withdrawals become tax free, they also became no longer included in “taxable income” and so didn’t need to be declared on tax forms.

This meant that many retirees on reasonable super incomes were no longer taxed at reasonable rates on their other income, including income from shares which could be untaxed if it fell below the tax free threshold.

And because of the 2001 decision to send dividend imputation cheques to shareholders who were untaxed, these retirees who suddenly found themselves untaxed also got imputation cheques mailed to them from the government.

Self-managed super funds, whose income is tax exempt in the retirement phase, also got imputation cheques.

In July 2017 the Turnbull government wound back tax free super by placing a limiting it to accounts with less than A$1.6 million. The restriction was to hit 1% of super-fund members.

Labor’s proposal

Treasury’s 2015 tax discussion paper prepared for the Abbott government referred to “revenue concerns” about dividend imputation cheques.

They cost the budget just A$550 million in the year the Howard government introduced them, but A$5 billion per year by 2018 and were on track to cost A$8 billion.

Labor’s proposal, announced in mid March 2018, was to return the divided imputation system to where it had been before Howard changed it in 2001, and to where it still is elsewhere. Tax credits could be used to eliminate a tax payment but not to turn it negative.

Labor allowed exceptions for tax exempt bodies such as charities and universities who would continue to receive imputation cheques alongside dividends.

Pensioner guarantee

Two weeks later, in late March, Labor amended its policy by adding a “pensioner guarantee”. Pension and allowance recipients, even part pensioners, would be exempt from the changes and would continue to receive cash payments.

Also exempt would be self-managed super funds with at least one member who was receiving a government pension or part-pension at the date of Labor’s announcement, 28 March 2018.

The change cost relatively little (the budget saving over the next four years fell to A$10.7 billion from A$11.4 billion) because most of the imputation cheques go to Australians with too much wealth to get even a part pension.

Self Managed Super Funds

Retail and industry super funds pool their members contributions, and so almost always have tax to reduce, meaning most would be unaffected by the withdrawal of cash credits.

Self Managed funds usually represent just one person, or a couple; their funds aren’t pooled with anyone else’s. This means that in the retirement phase, where fund earnings are untaxed, most do not have enough tax to reduce. So they get imputation cheques, which they would no longer get when Labor’s policy was implemented.

There is no such thing. The phrase is shorthand for Labor’s proposal to withdraw dividend imputation cheques from dividend recipients who are outside the tax system.

The Australian economy will remain healthy for long enough to enable the government to claim it as a strength in the lead-up to the May election, but the first Conversation Economic Survey points to a fairly flat outlook beyond that, with a 25% chance of a recession in the next two years.

The Conversation has assembled a forecasting team of 19 academic economists from 12 universities across six states. Among them are macroeconomists, economic modellers, former Treasury and Reserve Bank economists, and a former member of the Reserve Bank board.

Taken together their forecasts point to no recovery in the share market during 2019, no recovery in wage growth, no further improvement in the unemployment rate, further modest home price falls in Sydney and Melbourne, and to a budget deficit next financial year despite the official forecast of a surplus and Treasurer Josh Frydenberg’s commitment that the government will fight the election continuing to forecast a surplus.

Weighing heavily on Australia’s economy during 2019 will be a much weaker US economy, with what the forecasting team says is the possibility of a US recession, and weaker growth in China. Australian consumer spending is forecast to continue to grow during 2019, but no faster than it did during 2018. The best measure of living standards is forecast to advance at a crawl.

Most of the team expect the Reserve Bank to sit on its hands throughout all of 2019, leaving its cash rate unchanged at the all-time low of 1.5% for what will be a record 40 months.

Economic growth

The panel expects the Australian economy to grow more slowly in the year ahead, by 2.6%, down from recent annual growth of 2.8% and 3.1%. None of the panel expects growth to exceed 3%. One, Steve Keen, formerly of the University of Western Sydney and now at University College London, expects growth of only 1%.

Most of the panel expect China’s growth to continue to slow, from the annual growth of 6.7% typical over recent years to just 6.2%, the weakest growth since the 2008 global financial crisis and the weakest calendar year growth since 1990.

Former Treasury economist Nigel Stapledon now at the University of NSW nominates China as the biggest threat to Australian and global growth. He says it has a good record of stimulating its economy to get out of difficult corners but one day it might get it wrong.

The panel expects US economic growth to hold up at 2.8% during the year ahead but to weaken or go into reverse by year’s end as the “sugar hit” from the Trump tax cuts goes into reverse.

Former Treasury and International Monetary Fund economist Tony Makin points to US high public debt that will need to be rolled over, soaking up funds that could have been more productively used for investment, to higher US interest rates imposed by a central bank concerned about inflation, and to the escalating trade war with China.

ANU modeller and former Reserve Bank board member Warwick McKibbin says the US economy is “very likely” to begin to go backwards towards the end of the year. Craig Emerson, a former Australian trade minister now with Victoria University, says the US is likely to enter a recession in 2020. Former Treasury economist Mark Crosby at Monash University says if there is a US recession, it won’t hit until late 2019, with the impact greatest in 2020.

Rebecca Cassells from the Bankwest Curtin Economics Centre says a lot depends on the outcome of the US-China trade war: “The two biggest economies are going head to head, but both are almost as reliant on the other to sustain their growth trajectories,” she says.

Australia should look to other parts of the world to drive its economic growth. “India is one of them, and is rising rapidly with no downgrading of its growth trajectory of 7.75% for 2019.”

Living standards

Nominal GDP, the money earned in Australia unadjusted for price changes, is forecast to grow more slowly in 2019, by 4.5%, down from recent growth in excess of 5%, reflecting weaker iron ore prices.

The best measure of living standards, real net disposable income per capita, is expected to barely grow, climbing just 1% over the year to December, much less than recent growth in excess of 3%, but much more than its performance in the dismal years between 2012 and 2016 when it went backwards.

Forecasts for the unemployment rate cluster around its present 5.1%, with only four below 5% and one above 6%.

Wages and prices

Wage growth is forecast to climb no further in 2019, finishing the year at its present 2.3% instead of climbing to 2.75% on its way to 3% by mid 2020 as forecast in the budget update.

Rebecca Cassells points out that much of the increase we have had has been driven by the Fair Work Commission’s decision to lift the minimum wage 3.5% from June 2018, suggesting very low growth elsewhere. Disturbingly, she says more and more enterprise bargains are being terminated, with employees falling back on awards.

Overwhelmingly, our panel is of the view that the only thing that will lift wage growth out of its slump (and budgets have been incorrectly forecasting a bounce out of the slump for eight years now) is higher productivity: producing more per worker.

Victoria University economic modeller Janine Dixon notes that the December budget update actually downgraded its forecast of productivity growth, from 1.5% to 1%, and so is not optimistic.

She says even if productivity growth did pick up, excessive market power in some industries combined with weakness in labour market institutions means it might not easily be passed on to workers.

Tony Makin, a supporter of company tax cuts, says the best thing to lift productivity would be new (perhaps foreign) investment embodying productivity-enhancing technology.

The saving grace for workers facing yet another year of historically-low wage growth is that price increases will also remain low.

Inflation has been right at the bottom of (or below) the Reserve Bank’s 2% to 3% target band for four years now, meaning that even at the continuing low rates of wage growth forecast, wages should continue to climb just faster than prices.

The panel expects consumer spending to climb by only 2.5% in real terms in 2019, most of which will reflect population growth of 1.6%.

The average forecast for inflation is at the very bottom of the Reserve Bank’s target band. Only two panel members expect inflation to edge back up to the middle of the band. They are Warwick McKibbin and former Treasury and ANZ Bank chief economist Warren Hogan, at the University of Technology Sydney.

Interest rates and the budget

Without either a lift in inflation or a substantial weakening in the economy there is little reason for the Reserve Bank to move interest rates in either direction.

Governor Philip Lowe took the job in September 2016, just after the board cut the cash rate to a record low of 1.5%. He hasn’t moved the cash rate since, although on several occasions he has said the next move is most likely to be up.

Five of the panel do expect at least move up this year, including the two who think inflation might approach the bank’s target. Three expect cuts, taking the rate below 1.5%.

The remaining eleven expect no change, all year.

The government says it will deliver a budget surplus next financial year, of A$4.1 billion, the first surplus in a decade.

The panel doesn’t think so, all but one member predicting a lower budget surplus than the government, and seven predicting deficits. The average forecast is for a deficit of A$3.5 billion rather than a surplus of A$4.1 billion.

Monash University macroeconomist Solmaz Moslehi identifies optimistic wage growth, weaker than expected mining investment and a hit to consumer spending from the housing downturn as the biggest risks to the forecast surplus.

Julie Toth, adjunct professor at Deakin University’s Master of Business Administration program and chief economist at the Australian Industry Group, says the latest indicators suggest that neither employment nor wage growth will accelerate by as much as the government expects.

Michael O’Neil from the South Australian Centre for Economic Studies says the biggest immediate risk to the forecast surplus is thermal coal prices, given China’s efforts to cut coal imports and the shift to renewables in China and India.

The biggest long term risk is the scale of the company tax cuts and the ongoing shift of income from highly-taxed labour to more lightly-taxed capital.

Margaret McKenzie of Federation University identifies the biggest risk to the surplus as a change of government, something she says she welcomes because with extensive idle capacity and underemployment, a surplus would be unhelpful.

Home prices

The panel expects Sydney home prices to fall by another 5.8% and Melbourne prices by another 5.1% in 2019, taking the slides over two years to 14.7% and 12.1%.

Only Macquarie University and former Reserve Bank economist Jeffrey Sheen expects prices to move back up throughout 2019, by 2% and 3%.

Reassuringly, none of the forecast falls are bigger than 10%. The biggest are predicted by Steve Keen, Tony Makin, Margaret Mckenzie and Craig Emerson.

The lower prices will be accompanied by much slower growth in housing investment, expected to climb only 2.1% in 2019 after climbing more than 7% in the year to September 2018.

Business

Non-mining business investment is forecast to grow more slowly this year, by 5.7% instead of 11.4%, and mining investment is expected to keep sliding, losing a further 3.4% after losing 11.2% last year rather than climbing as the government’s budget update predicts.

Five of the team believe that mining investment to turn the corner in line with the budget forecast. Nine expect it to fall further.

The Australian share market will for practical purposes not grow not at all during 2019 according to the average forecast, which is for barely perceptible growth of 0.1%. A steady share market would come as a relief to super funds and share owners after last year’s slide of about 7%.

The range of forecasts for the ASX 200 is wide, from slides of more than 6% to gains of more than 6%.

Markets

Fortunately for a government the panel expects to need to continue to borrow more in order run continued budget deficits, what it pays for to borrow via the 10-year bond rate is expected to remain little changed at 2.6%. Only Warwick McKibbin expects a much higher bond rate, of 3.5%.

The panel’s average forecast is for an broadly unchanged Australian dollar, of around 70.5 US cents. The highest forecast is for US$0.80, the lowest for US$0.62.

The iron ore price, at present close to US$74 a tonne, is expected to fall to around US$64. Only one panelist, Warwick Mckibbin, expects it to stay near where it is, at US$75. The government itself is cautious, using a price of US$55 in its budget forecasts, a number it might lift in the April budget, allowing it to forecast more revenue.

The risk of recession

On average, the panel believes there is a 25% chance of a conventionally-defined recession within the next two years.

Half of the probability estimates are between 20% and 30%. Averaging all of them together other than Steve Keen’s estimate of 95% produces an estimate of 22%.

A recession is conventionally defined as two consecutive quarters in which gross domestic product falls instead of rises. Australia hasn’t had two consecutive quarters of negative growth since 1991.

The most recent negative quarter was in September 2016. Before that there was one in March 2011, and before that in during the global financial crisis in December 2008.

Ross Guest of Griffith University makes the point that his estimate of 20% should be considered low. There will always be a risk of a recession. By itself two quarters of negative growth needn’t be a disaster. The impacts on the government and on consumer and business confidence would be more important than the downturn itself.

Guay Lim of the Melbourne Institute of Applied Economic and Social Research assigns the lowest probability of any of our panel to a recession, 5%, saying the most likely catalyst would be a global trade war.

Warren Hogan assigns the highest probability to a recession after Steve Keen, 40%, saying Australia is facing the end of a major construction boom and has heavily indebted households. It will be vulnerable to any negative shocks and especially vulnerable to higher inflation and interest rates.

Steve Keen says the only thing that has kept Australia afloat since the China boom has been the housing bubble, which the banking royal commission has been discovering was built on fragile, and in places fraudulent, foundations.

Nigel Stapledon says the biggest drag on the economy will be the collapse in the construction of residential investment units. Labor’s proposed increase in capital gains tax will make it worse, notwithstanding Labor’s decision to exempt new construction from its crackdown on negative gearing.

Rebecca Cassells says on the bright side Australia is set to become the world’s biggest exporter of liquefied natural gas, the biggest exporter of iron ore to India and the world’s biggest producer of lithium, needed for batteries.

And if there is a global economic downturn within the next few years, she says another positive is that Labor is likely to be in power, making the successful deployment of a stimulus package more likely than if the Coalition had been in office.

Want more to retire on?

In its long-awaited final report on the efficiency and competitiveness of Australia’s leaky superannuation system, Australia’s Productivity Commission provides a roadmap.

Weeding out scores of persistently underperforming funds, clamping down on unwanted multiple accounts and insurance policies, and letting workers choose funds from a simple list of top performers would give the typical worker entering the workforce today an extra A$533,000 in retirement.

Even Australians at present in their mid fifties would gain an extra A$79,000.

If this government or the next cares about the welfare of Australians rather than looking after the superannuation industry it’ll use the recommendations to drive retirement incomes higher.

So why the continued talk (from Labor) about lifting compulsory super contributions from the present 9.5% of salary to 12%, and then perhaps an unprecedented 15%?

It’s probably because (and Paul Keating, the former treasurer and prime minister who is the father of Australia’s compulsory superannuation system says this) they think the contributions don’t come from workers, but from employers.

To date, they’ve been dead wrong. And with workers’ bargaining power arguably weaker than in the past, there’s no reason whatsoever to think they’ll be right from here on.

Past super increases have come out of wages

Australia’s superannuation system requires employers to make the compulsory contributions on behalf of their workers. Right now that contribution is set at 9.5% of wages and is scheduled to increase incrementally to 12% by July 2025.

So, for workers, what’s not to like?

It’s that while employers hand over the cheque, workers pay for almost all of it via lower wages. Bill Shorten, then assistant treasurer, made this point in a speech in 2010:

Because it’s wages, not profits, that will fund super increases in the next few years. Wages are the seedbed of the whole operation. An increase in super is not, absolutely not, a tax on business. Essentially, both employers and employees would consider the Superannuation Guarantee increases to be a different way of receiving a wage increase.

The Henry Tax Review and other investigations have found this is exactly what happens. Increases in the compulsory super contributions have led to wages being lower than they otherwise would have been.

Even Paul Keating, speaking in 2007, made this point. Compulsory super contributions come out of wages, not from the pockets of employers:

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost […] In other words, had employers not paid nine percentage points of wages, as superannuation contributions, they would have paid it in cash as wages.

This is more than mere theory. Compulsory super was designed to forestall wage rises. Concerned about a wages breakout in 1985, then Treasurer Paul Keating and ACTU President Bill Kelty struck a deal to defer wage rises in exchange for super contributions.

When the Super Guarantee climbed from 9% to 9.25% in 2013, the Fair Work Commission stated in its minimum wage decision of that year that the increase was “lower than it otherwise would have been in the absence of the super guarantee increase”.

The pay of 40% of Australian workers is based on an award or the National Minimum Wage and is therefore affected by the Commission’s decisions. For these people, there is no question: their wages are lower than they would’ve been if super hadn’t increased.

Where’s the evidence employers pay for super?

If wage rises came from the pockets of employers then we should see a spike in wages plus super when compulsory super was introduced, and again when it was increased. But there wasn’t one when compulsory super was introduced – a point Bill Shorten has made in the past.

When compulsory super was introduced via awards in 1986, workers’ total remuneration (including super) made up 63.3% of national income. By 2002, when the phase-in was complete, it made up 60.1%.

Out of the 26 countries for which the Organisation for Economic Co-operation and Development has data, Australia recorded the tenth largest slide in the labour share of national income during the period compulsory super contributions were ramped up.

Of course, changes in super aren’t the only thing that affects workers’ share of national income.

But the size of the fall in the labour share in Australia over the period when the super guarantee was increasing isn’t consistent with the idea that employers picked up the tab for super.

Would it be different this time?

Paul Keating argues that while in the past lifting compulsory super to 9.5% was paid for from wages, a future increase to 12% today would not be:

Workers are not getting real wage increases anywhere, and can’t get them. The Reserve Bank governor makes the point every week. So the award of an extra 2.5% of super to employees via the super guarantee will give them a share of productivity they will not get in the market – without any loss to their cash wages.

But such claims are difficult to square with concerns that workers’ weak bargaining power is one of the reasons current wage growth is so weak.. If employers don’t feel pressed to give wage rises, why would they feel pressed to absorb an increase in the compulsory Super Guarantee?

And while real wages (wages adjusted for inflation) haven’t grown particularly quickly, the dollar value of wages continues to grow: by 2.2% a year over the past five years. It would be easy for employers to simply reduce those increases to offset any increase in compulsory super – as they have in the past.

And no, more contributions won’t help workers

The Grattan Institute’s recent report, Money in Retirement, showed increasing the compulsory super would primarily benefit the top 20% of Australians. It would hurt the bottom half during working life a lot more than it helps them once retired.

Their higher super contributions would not improve their retirement outcomes: their extra super income would be largely offset by lower part-pensions. What’s more, the age pension is indexed to wages. If wages grew by less (as they would as compulsory super contributions were increased) pensions would grow by less too.

Lifting compulsory super would also cost the budget A$2 billion a year in extra tax breaks, largely for high-income earners, because it is lightly taxed.

That would mean higher taxes elsewhere, or fewer services.

For low-income Australians, increasing compulsory super contributions would be a thoroughly bad deal. It means giving up wage increases in return for no boost in their retirement incomes.

A government that wanted to boost the living standards of working Australians both now and in retirement would consider carefully all of the Productivity Commission’s suggestions including this one: an independent inquiry into the whole idea and effectiveness of Australia’s regime of compulsory contributions, to be completed ahead of any increase in the Superannuation Guarantee rate .