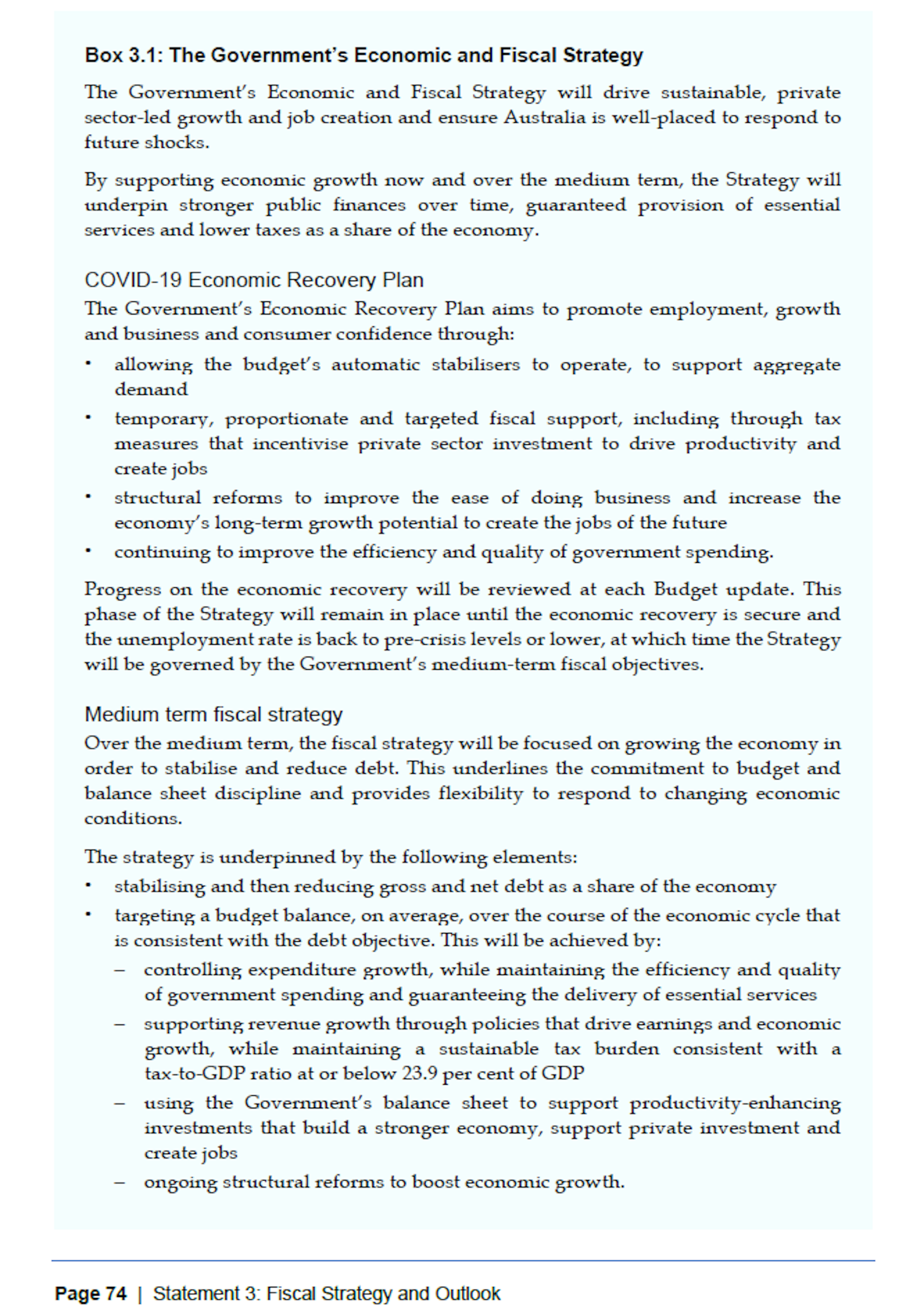

If you are anything like me, the nearer you get to a deadline, the more desperately you want to postpone it, no matter how much harder that makes things down the track.

It’s what the Coalition wants Australia to do about its 2030 emissions reduction target – the one signed into law in 2022 and registered with the United Nations Framework Convention on Climate Change.

The Coalition says it remains “fully committed” to the more challenging target of net zero by 2050, but it wants to postpone some of the work needed to achieve it until later, nearer 2050.

It’s a human impulse that until the 1980s had economists baffled. That’s when they came up with a new name for it: “hyperbolic discounting”.

Most of us put things off

Before then, economists had no problem explaining people putting things off. We’d long had the concept of a “discount rate” to explain why we do it.

If I offered you a choice of finishing an unpleasant task this month in return for $100, or finishing it a year later for 5% less, you are pretty likely to opt for finishing it a year later in return for 5% less.

Economists would say that meant your “discount rate” (the rate at which you discount what happens in the future) was greater than 5% per year.

It’s an incredibly useful concept, and one of the reasons we want to be paid interest when we lend money or deposit money in a fixed-term account.

Yes, it will be nice to get our money back – but getting it back when the loan ends won’t feel as good as having it now. If our discount rate is 5% per year, getting the full amount back then will be worth 5% less to us per year, so we will want interest of 5% per year.

Voters and politicians discount the future

It’s also how governments and businesses decide whether to fund major projects. If their discount rates are 5% (they are usually higher) and the eventual payoff from the project works out at less than 5% per year, it isn’t worth it. As a species, we are more concerned about what happens now than what happens in the future.

At least that’s what was taught at universities in 1970s: everyone has their own personal discount rate. For patient people it is low, and for impatient people it is higher. If you can find out what it is, you can find out what they should do.

Except that many of us don’t behave like that at all. We appear to have a discount rate, but it changes – dramatically – the closer we get to a deadline.

Near deadlines, our behaviour becomes extreme

Remember when I asked about finishing an unpleasant task this month or a year later? You might well have given an answer that implied a discount rate near 5%.

You would have probably given a similar answer if I asked about finishing the task a year after that, in 2027 instead of 2026. Your discount rate would be near 5%.

Except for the week before the task is due. In that week, you might well be prepared to sacrifice almost anything – an awful lot – to put it off for another week or another month, or two months or a year. Your discount rate would be off the charts.

On a chart, it wouldn’t look like a straight line – 5% or so per year – it would like a hyperbola, a line that had suddenly climbed enormously high. That has also been used to describe the concept of hyperbolic discounting.

Acting like a hyperbolic discounter – pushing out a deadline as it becomes imminent, even if it costs more to meet it later – as the Coalition now says it will do the 2030 emissions reduction target, is a way to never meet a deadline.

Of course, the Coalition says it won’t cost more to meet the final deadline of net-zero by 2050 because by then we will have nuclear power.

It’s a familiar argument to those of us who want to put things off. Something will come along that will make them easier to do later. If it doesn’t, maybe we will behave like a hyperbolic discounter again. Not that we expect to.

Nuclear power mightn’t make future choices easier

Except that the unexpected happens. Cost overruns are notorious in building nuclear power plants, even in countries that have lots of them and they are often delivered late.

And electricity is responsible for only one-third of Australia’s greenhouse gas emissions. Cutting electricity emissions to zero (a road we are already on, they’ve been falling since 2015) will leave another two-thirds of emissions untouched.

That’s unless we rapidly electrify other sources of emissions such as cars and trucks and the use of gas for heating, a transition the Coalition remains reluctant to embrace.

It’s hard to meet deadlines. Right now the government is on track to miss its 2030 emissions target of 43% below 2005 levels, although its officials say it is on track for 42% and it thinks it can make up the difference.

It’s tempting to put things off. If the Coalition persuades us, it’s because we are highly persuadable. Most of us don’t like hard choices now. We like them later.![]()

This article is republished from The Conversation under a Creative Commons license. Read the original article.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}