The economy bounced back from last year’s COVID recession far more sharply than the treasury (or just about anyone else) expected.

The bounty from the higher-than-expected tax collections that flowed from more people than expected in work, a much higher-than-expected iron ore price, and lower than expected unemployment benefits, should amount to A$26.8 billion this financial year, $15.5 billion the next, and $18.6 billion the year after that.

But rather than bank those riches and improve the budget bottom line, as the Coalition’s budget strategy used to require it to do, the government has instead decided to spend the lot.

It will spend $21 billion of this year’s $26.8 billion; it will spend or give up in new tax concessions $26.9 billion — far more than next year’s $15.5 billion bounty, and so on.

Treasurer Josh Frydenberg has come good on his historic promise to keep spending way beyond the crisis, to drive the unemployment rate down below where it was when the pandemic started.

Read more: View from The Hill: Frydenberg finds the money tree

The budget predicts an unemployment rate of 4.75% by mid-2023 and 4.5% by mid-2024.

If delivered (and the treasurer’s revised strategy published in the budget requires him to keep spending until it is), it will mark what the budget papers describe as, “the first sustained period of unemployment below 5% since before the global financial crisis, and only the second time since the early 1970s”.

In the same way as Australia emerged from the early-1990s recession with a dramatically lower inflation rate because the Reserve Bank was determined to salvage something from the carnage, Frydenberg has decided to exit the COVID recession with an ongoing lower floor under unemployment.

Both the treasury and Reserve Bank believe Australia can sustain much lower unemployment than the 5-6% it has grown used to. The treasury’s estimate is 4.5%; the Reserve Bank’s is nearer 4%. Before COVID, the United States managed 3.5%.

Read more: Fewer hard hats, more soft hearts: budget pivots to women and care

If achieved, it will mean hundreds of thousands more Australians providing services, drawing paycheques, and paying tax. And no longer on benefits.

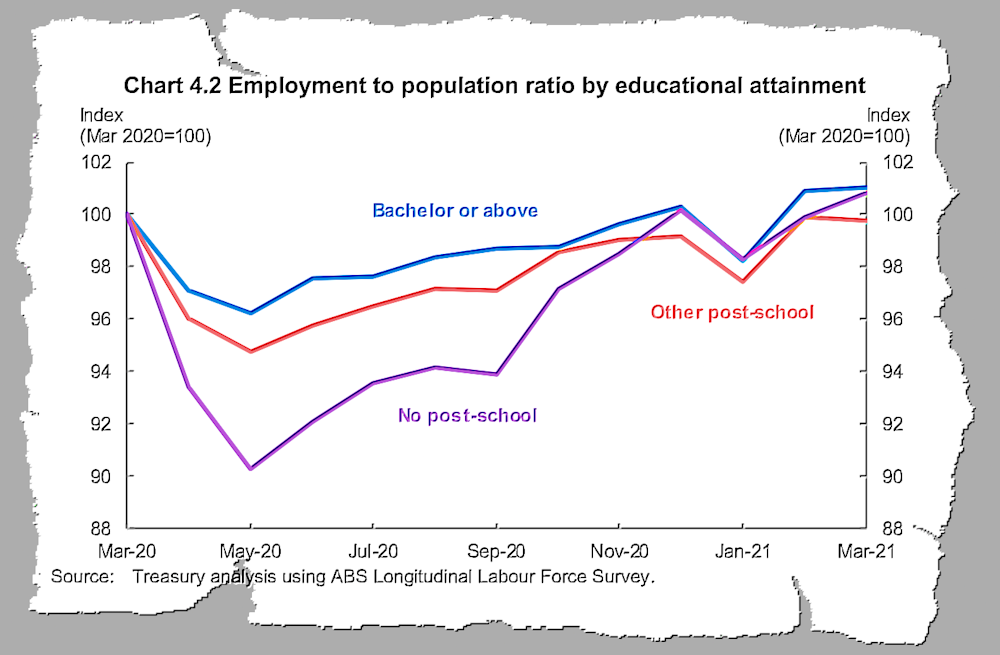

A dramatic budget graph tracking the fortunes of every Australian whose payroll was reported to the tax office throughout 2020 shows the biggest victims of the COVID recession — by far — were those without post-school education. At the deepest point of the COVID recession in May, they were almost three times as likely to have lost their jobs as Australians with degrees.

The budget provides an extra $400 million for low-fee or no-cost training for jobseekers, to be matched by the states; an extra $481 million for the transition to work employment service directed at Australians aged 24 and under; and a further $2.4 billion to the Boosting Apprenticeship Commencements program.

But most of what it intends to do for jobs is the indirect result of a barely precedented expansion in spending and tax concessions in all sorts of areas.

The extra $17.7 billion it is spending on aged care over four years ought to create many jobs, as should the extra $13.2 billion it is spending on the National Disability Insurance Scheme.

The $1.7 billion it is spending on making childcare more affordable should both create jobs in the sector and free up more parents to return to work.

Read more: Cuts, spending, debt: what you need to know about the budget at a glance

An extra $20 billion in business tax concessions should help as well.

The budget’s break with the past isn’t its dramatic expansion of discretionary spending. That’s common in recessions. What’s unusual is that spending is being ramped up when we are not in recession.

In the words beloved of economists, the spending is “pro-cyclical” rather than “counter-cyclical”. It is designed to supercharge our exit from recession rather than merely bring it about.

And there’s little sign of the spending stopping.

If this government or the next achieves success in driving the unemployment rate down to 4.5%, it will want to go further. It will keep going further right up until we get inflation near the top of the Reserve Bank’s 2-3% target band and wage growth in excess of 3%, neither of which this budget foresees in forecasts going out four years.

Government debt, anathema to the Coalition when Labor ran it up during and after the global financial crisis, isn’t much of a constraint.

Read more: Josh Frydenberg has the opportunity to transform Australia, permanently lowering unemployment

The Reserve Bank holds much of the government’s debt (it didn’t during Labor’s time) and is buying as much as it needs to to keep interest rates low. Recently, interest rates have been rising, but not for most of the government’s borrowings, which are long-term.

The budget papers show that even with net government debt at 34% of GDP and heading to 44%, interest payments on that debt are much less of a drain on the budget than they were back in the mid 1990s when net debt hit 18% of GDP.

And the times have changed. Worldwide, few nations have an aversion to government debt, especially not the United States. In Australia, the only side of politics that used to complain about debt is in currently in office.

Before COVID, the fiscal strategy spelled out in the budget as part of the Charter of Budget Honesty required the government to eliminate net debt.

Frydenberg’s revised strategy merely requires him to stabilise and then reduce net debt “as a share of the economy”.

His priority is driving down unemployment. If that helps expand the economy and so drives down net debt as a share of the economy so much the better. But he wants to do it regardless.

Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

This article is republished from The Conversation under a Creative Commons license. Read the original article.